Nuclear Monitor #921

Gerard Brinkman, WISE Netherlands

Nuclear power plant construction is not business as usual in a privatised energy market. Governments regularly intervene heavily, either through direct financing, providing loans and guarantees, or via risk-sharing and interference with price measures. This raises the question of how much a government will have to pay when planning a new nuclear power plant. Based on recent examples, what is the range of cost estimates that can be expected?

To this end, in a study by Dutch investigator Jeroen Walstra from Profundo a detailed analysis of the actual costs and timelines of typical and recent large-scale construction projects of new nuclear power plants is provided.

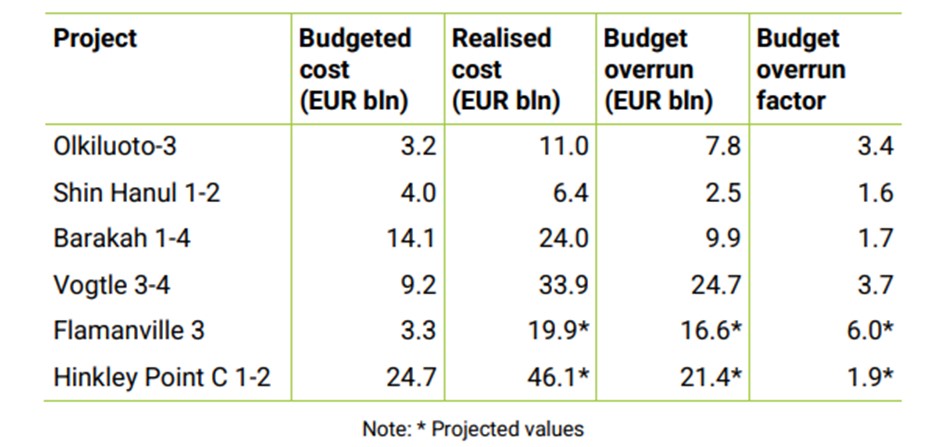

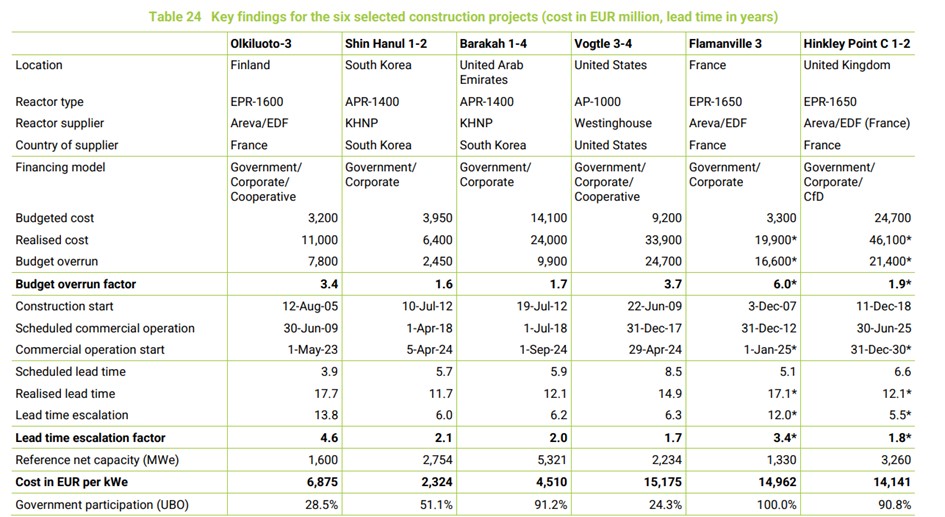

Six nuclear power plants have been selected for this research. They are among the latest to be put into operation globally:

- Olkiluoto 3 (Finland),

- Shin Hanul 1-2 (South Korea),

- Barakah 1-4 (United Arab Emirates),

- Vogtle 3-4 (United States),

- Flamanville 3 (France) and

- Hinkley Point C 1-2 (United Kingdom).

The six power plants use Generation III+ Pressurized Water Reactors. The technologies are from France, the US and South Korea. This matches the technology choices the Dutch government is exploring.

The outcome of the research is compared to the proposals for Borssele 2-3 and Dukovany 5-6. The latter is a Czech project for which the preferred bidder has just recently been chosen: Korea Hydro & Nuclear Power Company (KHNP), the nuclear subsidiary company of Korea Electric Power Corp (KEPCO). This is an interesting example because, on the one hand, KEPCO has shown its ability to realise nuclear construction projects domestically in South Korea, at cost-competitive prices. On the other hand, its bidding price for the project in Europe lies considerably higher, almost a factor of 4. This may point to additional costs caused by first-of-a-kind characteristics.

The research conducted for WISE calculated factors for both budget overruns and lead time escalations. Both these exceedances are expressed in multiplication factors, to emphasise how many times the initially planned construction cost and construction period have gone over the top. Based on the data of the six construction projects case studies, the calculated factors are:

The identified realised construction costs (in EUR billion) are:

The identified realised construction lead times (in years) are:

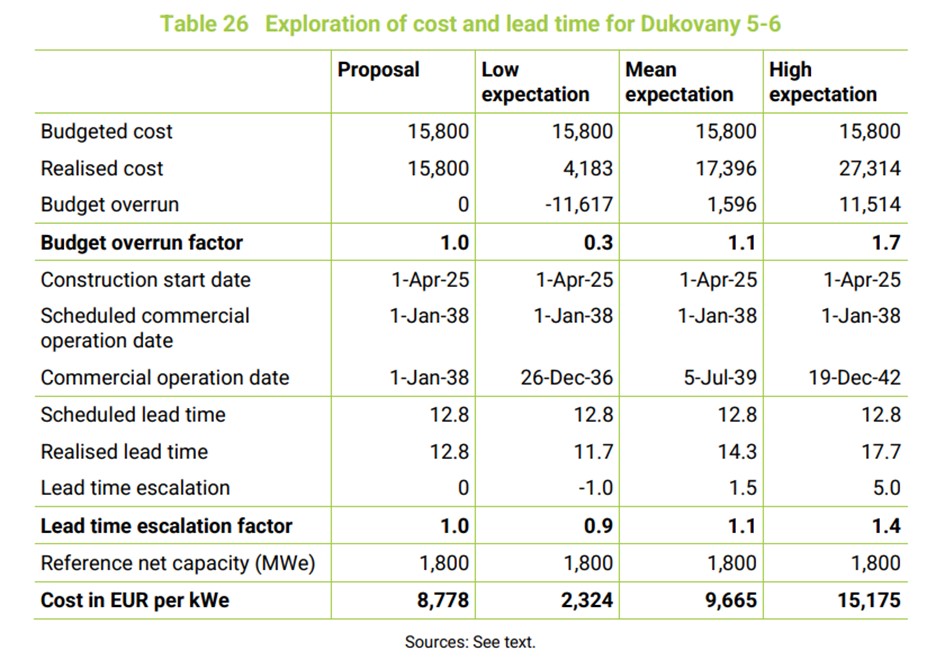

Based on the results from the six case studies, it has been calculated what this would mean for the preparation of Dukovany 5-6 and Borssele 2-3.

According to the Dukovany 5-6’s bid, the project is budgeted at EUR 15.8 billion and a lead time of 12.8 years. The analysis shows that this initially budgeted cost is close to the

mean value that is expected based on the case studies. The calculated low expectation is considered unrealistic and ruled out. The mean expectation would be a realised cost of EUR 17.4 billion and a budget overrun factor of 1.1. The high expectation would be a realised cost of EUR 27.3 billion with a budget overrun factor of 1.7.

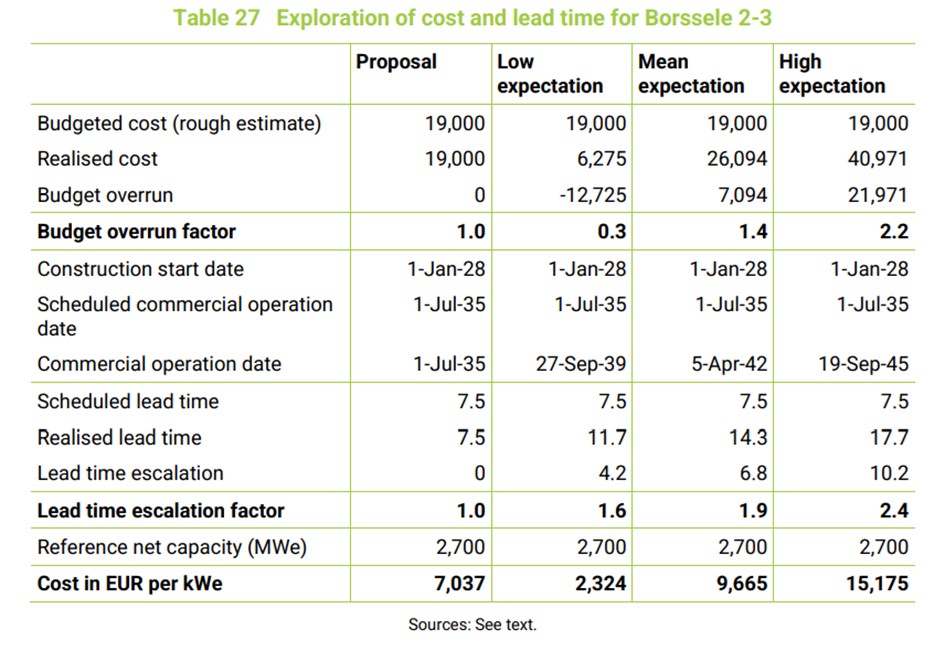

For Borssele 2-3 a cost estimate is not available yet. The Dutch government intends to make a reserve of EUR 7 billion (for two units), but the financing model has not been chosen, and the proposed budget reserve is awaiting parliamentary approval. Therefore, the analysis took a rough estimate of the available budget (EUR 19 billion) based on the proposed reserve to enable the exploration of the expected cost range. An initial schedule mentions Borssele 2-3 to start operations in July 2035.

The calculated low expectation is considered unrealistic and ruled out. The mean expectation would be a realised cost of EUR 26.1 billion and a budget overrun factor of 1.4. The high expectation would be a realised cost of EUR 41.0 billion with a budget overrun factor of 2.2

Financing models

Several financing models have been found. All six cases have a mix of corporate and government financing. Barakah 1-4 and Flamanville 3 have the highest share of government contributions. Olkiluoto 3 and Hinkley Point C 1-2 the lowest. Olkiluoto 3 and Vogtle 3-4 have a cooperative financing model in which the power off-takers participate. In Finland, this is called the Mankala model, and the participants are both corporations and governments. In the US, the participants are also corporations and governments, but also customer cooperatives. Government price regulation in the form of a Contract for Difference, which guarantees the operator a minimum price, supports the financing of Hinkley Point C 1-2. A price measure is not known for the other five cases. The proposed Dukovany 5-6 project takes three (EU-approved) price measures: direct price support via a power purchasing agreement (PPA), a two-way Contract for Difference, and a partly closed price market (30%) through government auctioning.

The study analysed the government contribution to the financing of the six selected construction projects. This has led to some remarkable observations:

- In the Olkiluoto and Hinkley Point cases, the financial contribution of the domestic governments (Finland and the UK, respectively) was limited, while the contribution of foreign governments was significant. In literature, this is sometimes called government-to-government financing, but a more accurate term is government-supported vendor financing. In the mentioned cases, the governments support the export opportunities in favour of their national nuclear sector.

- Remarkably, this has come at a considerable price, especially for the French government, which had to restructure and nationalise Areva and EDF.

- Furthermore, especially in the cases of Olkiluoto, Hinkley Point and Vogtle, the domestic government turned out to be more involved in the financing than it was thought. This is caused by governments owning significant company shares through their ultimate beneficial ownership of the project sponsors, which is not visible at first sight.

- Due to EDF’s nationalisation and its presence in three of the case studies, these projects started with a larger corporate share of equity and ended up with a larger government share of equity.

- The financing of Barakah 1-4 may be described as nearly pure government financing. The government financing of Shin Hanul 1-2 is set at 51%, following the government share in KEPCO. However, as the Government of South Korea is the majority owner, KEPCO is statecontrolled and, therefore, the financing decisions of Shin Hanul 1-2 are in the hands of the government.

- The financing of Flamanville 3 may be described as a mix of government and corporate financing, with the government share getting larger in time, due to the covering of losses, shareholders buy-out and nationalisation. Part of the losses were also borne by the shareholders in the form of missing out on dividend payments and the loss of shareholder value. Although fully government-owned, EDF is a corporation, and part of the losses have been covered by internal accounting at the expense of returns of operations of other business activities. Also, a part of the financing has been provided by commercial lenders.

- The realised construction cost per installed kWe varies from EUR 2,324 to 15,175 per kWe. There is no clear relationship between government participation and lower costs.

- The government’s participation in the ultimate beneficial ownership of the project companies varies from roughly a quarter (24.3% of Vogtle 3-4) to full ownership (100% of Flamanville 3). Remarkable is the large government participation in the projects in France and the UK. Also remarkable is the government participation in the projects in Finland (24.3%) and the US (24.3%), which have only private companies as project sponsors. On average, government participation (UBO) is 64.3%.

For Dukovany and Borssele, the cost per kilowatt (electric) is taken from the case studies and varies from EUR 2,324 (low) to 9,665 (mean) and 15,175 (high expectation). The Dukovany bid translates into EUR 8.778 and the Borssele rough budget estimate into EUR 7,037 per kilowatt (electric).

The International Energy Agency (IEA) uses a value of EUR 6,230 per kWe for nuclear in its scenarios. A 2021 KPMG study identified an average cost per kW installed capacity of EUR 4,973 per kW. The 2022 Witteveen+Bos study identified an average cost of EUR 7,959 per kW but applied a cost of EUR 3,520 per kW in its scenarios. Since the current research identified a mean cost of EUR 9,665 per kWe, it is clear that updating the actual cost of the six projects was necessary. This outcome provides the opportunity to update, reassess, and improve the cost estimates for Borssele 2-3. Higher cost estimates may also lead to changed insights into cost-effectiveness by comparing scenarios of the future energy mix.

The costs per kilowatt (electric) for renewable energy sources range from 1,050 (solar PV) to 1,850 (wind onshore) and 3,620 (wind offshore). The study identified a mean cost per kilowatt (electric) for nuclear power plants of EUR 9,665. This price difference makes solar and wind highly favourable compared to nuclear when considering cost efficiency, lead times and financial risk.

Profundo identified an average construction lead time of 14.3 years. The expected construction lead times for Dukovany and Borssele are taken from the case studies and are in the range of 11.7 (low) to 17.7 years (high expectation). For Dukovany 5-6 this would result in a commercial operation date between December 2036 and December 2042; and for Borssele 2-3 a commercial operation date between September 2039 and September 2045.

A new nuclear power plant will come too late to result in carbon savings that will contribute to the climate targets for 2040 and earlier. Clearly, a contribution to the 2035 target of carbon-neutral electricity production in the Netherlands is out of sight. Potentially, Borssele 2-3 could contribute to reaching the 2050 climate targets. Whether this may be a significant contribution is a question open to further research.

Source :

Profundo. (2024 27 September). Financing new nuclear Governments paying the price?